System of Quality Management Resources

Advisory Services for Public Company Auditors

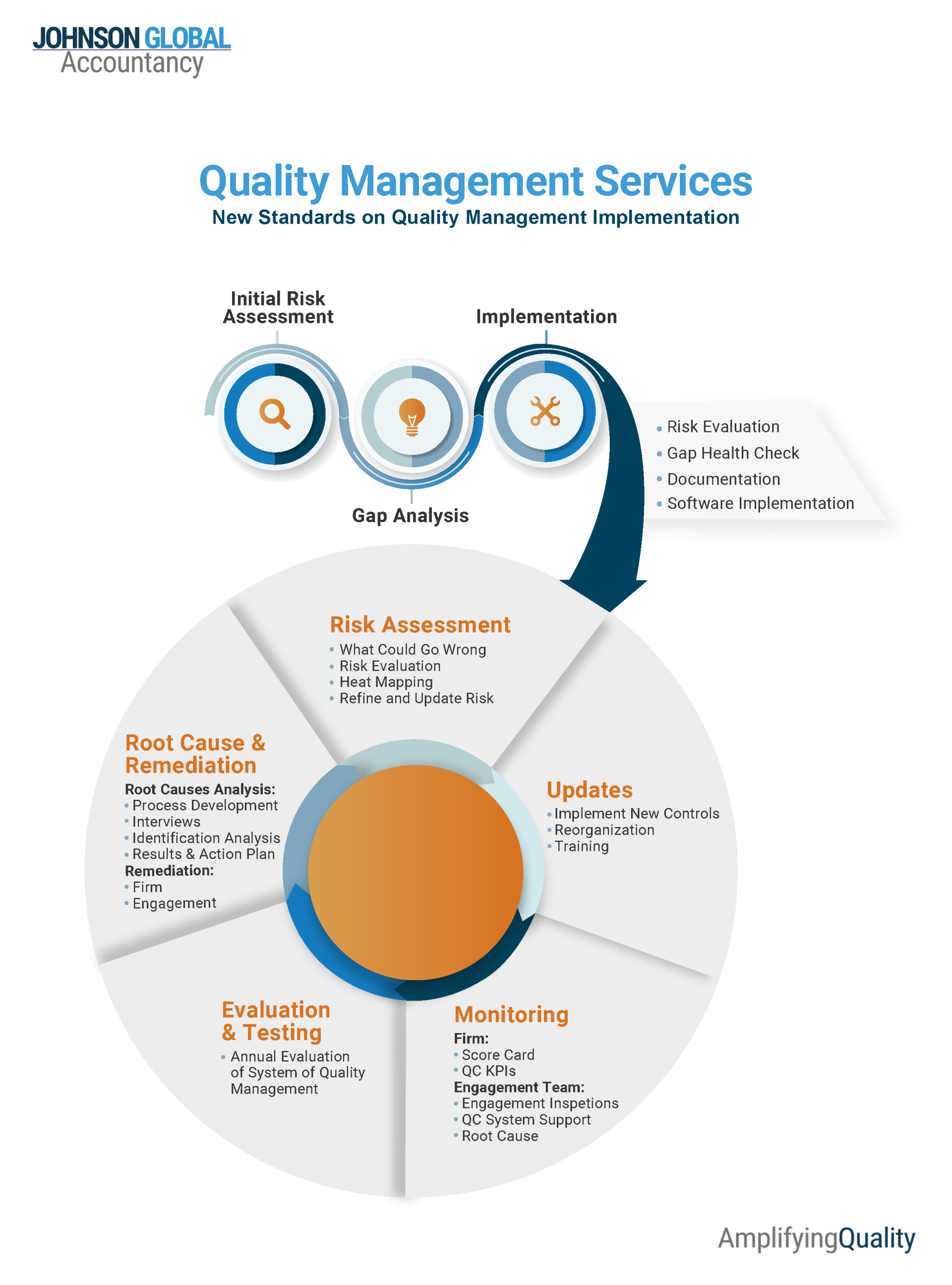

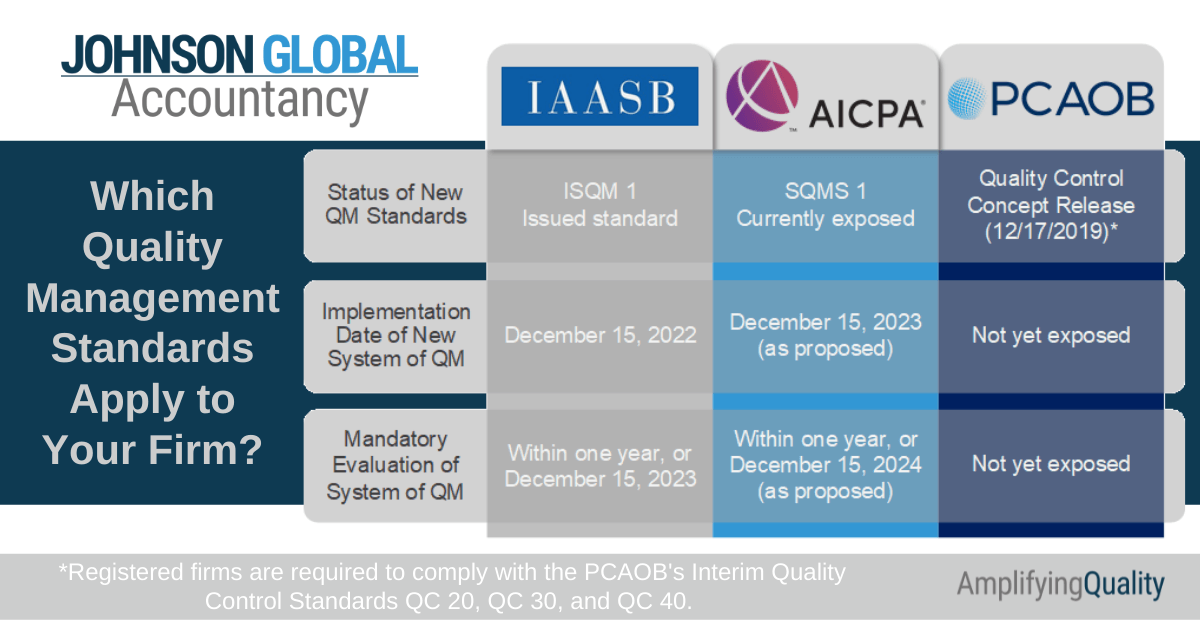

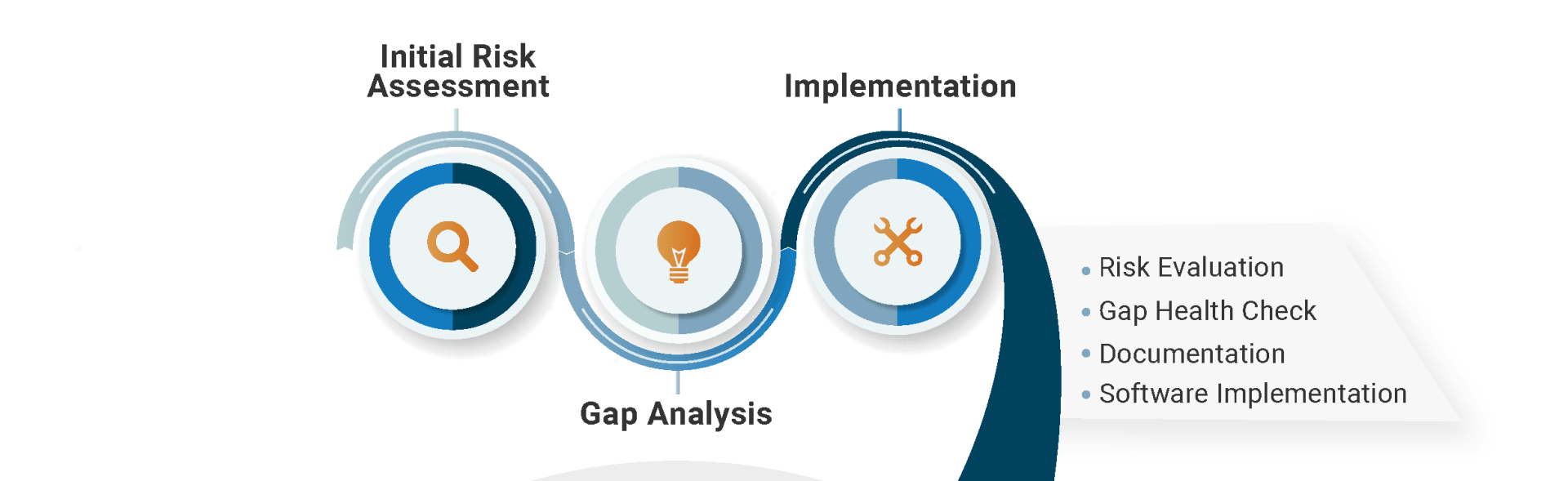

New QC Standards Readiness and Implementation

The International Auditing and Assurance Standards Board (IAASB) has adopted the new International Standard on Quality Management 1 (ISQM 1). In addition, the PCAOB has indicated its intention to issue new quality control (QC) standards in the near future. As a result, firms that are required to follow IAASB or PCAOB standards need to reconsider their internal quality controls and begin to implement new processes to comply with these new requirements.

Preparation and Assessment Process

Risk Assessment

- The firm’s process of implementing the risk-based approach to quality management.

- Consists of establishing quality objectives, identifying and assessing quality risks and designing and implementing responses to quality risks.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

- Design and implement a risk assessment process (Ref: Para. A39–A41)

- Establish the quality objectives specified by this ISQM and any additional quality objectives considered necessary (Ref: Para. A42–A44)

- Identify and assess quality risks to provide a basis for the design and implementation of responses. In doing so, the firm shall:

- Obtain an understanding of the conditions, events, circumstances, actions or inactions that may adversely affect the achievement of the quality objectives. (Ref: Para. A45–A47)

- Consider how, and the degree to which, the conditions, events, circumstances, actions or inactions in paragraph 25(a) may adversely affect the achievement of the quality objectives. (Ref: Para. A48)

- Design and implement responses to address the quality risks (Ref: Para. A49–A51)

- Establish policies or procedures that are designed to identify information that indicates additional quality objectives. (Ref: Para. A52–A53)

Governance & Leadership

Deals with matters such as the:

- Firm’s culture

- Leadership responsibility and accountability

- The firm’s organizational structure

- Assignment of roles and responsibilities, and

- Resource planning and allocation.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address the firm’s governance and leadership:

- Demonstrates a commitment to quality through a culture that exists throughout the firm, which recognizes and reinforces: (Ref: Para. A55–A56)

- Serving the public interest by consistently performing quality engagements;

- Importance of professional ethics, values and attitudes;

- Responsibility of all personnel for quality relating to the performance of engagements; and

- Importance of quality in the firm’s strategic decisions/actions including financial and operational priorities.

- Leadership is responsible and accountable for quality. (Ref: Para. A57)

- Leadership demonstrates a commitment to quality through their actions and behaviors. (Ref: Para. A58)

- Organizational structure & assignment of roles, responsibilities, and authority is appropriate to enable the design, implementation, & operation of firm system of quality management. (Ref: Para. A32, A33, A35, A59)

- Resource needs, including financial resources, are planned for and resources are obtained, allocated or assigned in a manner that is consistent with the firm’s commitment to quality. (Ref: Para. A60–A61)

Ethical Requirements

- Deals with fulfilling relevant ethical requirements by the firm, its personnel, and ethical requirements that apply to others external to the firm.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address the fulfillment of responsibilities in accordance with relevant ethical requirements, including those related to independence: (Ref: Para. A62–A64, A66)

- The firm and its personnel:

- Understand the relevant ethical requirements to which the firm and the firm’s engagements are subject; and (Ref: Para. A22, A24)

- Fulfill their responsibilities in relation to the relevant ethical requirements to which the firm and the firm’s engagements are subject.

- Others, including the network, network firms, individuals in the network or network firms, or service providers, who are subject to the relevant ethical requirements to which the firm and the firm’s engagements are subject:

- Understand the relevant ethical requirements that apply to them; and (Ref: Para. A22, A24, A65)

- Fulfill their responsibilities in relation to the relevant ethical requirements that apply to them.

Acceptance & Continuance

Deals with the firm’s judgments about whether to accept or continue a client relationship or specific engagement.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address the acceptance and continuance of client relationships and specific engagements:

- Judgments by the firm about whether to accept or continue a client relationship or specific engagement are appropriate based on:

- Information obtained about the nature and circumstances of the engagement and the integrity and ethical values of the client (including management, and, when appropriate, those charged with governance) that is sufficient to support such judgments; and (Ref: Para. A67–A71)

- The firm’s ability to perform the engagement in accordance with professional standards and applicable legal and regulatory requirements. (Ref: Para. A72)

- The financial and operational priorities of the firm do not lead to inappropriate judgments about whether to accept or continue a client relationship or specific engagement. (Ref: Para. A73–A74)

Engagement Performance

- Deals with the firm’s actions that support consistent quality engagements through direction, supervision and review, consultation, and differences of opinion.

- Includes how the firm supports engagement teams in exercising professional judgment and professional skepticism.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address the performance of quality engagements:

- Engagement teams understand and fulfill their responsibilities in connection with the engagements, including, as applicable, the overall responsibility of engagement partners for managing and achieving quality on the engagement and being sufficiently and appropriately involved throughout the engagement. (Ref: Para. A75)

- The nature, timing and extent of direction and supervision of engagement teams and review of the work performed is appropriate based on the nature and circumstances of the engagements. (Ref: Para. A76–A77)

- Engagement teams exercise appropriate professional judgment and professional skepticism. (Ref: Para. A78)

- Consultation on difficult matters is undertaken and conclusions are implemented. (Ref: Para. A79–A81)

- Differences of opinion within the engagement are communicated and resolved. (Ref: Para. A82)

- Documentation is assembled timely after the date of the engagement report. (Ref: Para. A83–A85)

Resources

- Deals with obtaining, developing, using, maintaining, allocating and assigning resources in a timely manner to enable the design, implementation and operation of the SQM.

- Includes 1) technological, 2) intellectual, 3) human resources, and 4) service providers.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address appropriately obtaining, developing, using, maintaining, allocating and assigning resources in a timely manner: (Ref: Para. A86–A87, A95–A97)

Human Resources

- Personnel are hired, developed and retained and have the competence and capabilities to achieve quality objectives (Ref: Para. A88–A90); demonstrate a commitment to quality and are held accountable (Ref: Para. A91–A93); and individuals are obtained from external sources when needed to achieve quality objectives. (Ref: Para. A94)

Technological Resources

- Appropriate technological resources are obtained or developed, implemented, maintained, and used, to enable the operation of the firm’s system of quality management and the performance of engagements. (Ref: Para. A98–A101, A104)

Intellectual Resources

- Appropriate intellectual resources are obtained or developed, implemented, maintained, and used, to enable the operation of the firm’s system of quality management. (Ref: Para. A102–A104)

Service Providers

- Human, technological or intellectual resources from service providers are appropriate for use in the firm’s system of quality management and in the performance of engagements. (Ref: Para. A105–A108)

Information & Communication

- Deals with obtaining, generating or using information regarding the SQM, and communicating information within the firm and to external parties on a timely basis to enable the design, implementation, and operation of the SQM.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish the following quality objectives that address obtaining, generating or using information regarding the system of quality management: (Ref: Para. A109)

- The information system identifies, captures, processes and maintains relevant and reliable information that supports the system of quality management, whether from internal or external sources. (Ref: Para. A110–A111)

- The culture of the firm recognizes and reinforces the responsibility of personnel to exchange information with the firm and with one another. (Ref: Para. A112)

- Relevant and reliable information is exchanged throughout the firm, including: (Ref: Para. A112)

- Information sufficient to fulfil responsibilities relating to the system of quality management; and

- Information when performing activities within the system of quality management or engagements.

- Relevant and reliable information is communicated to external parties, including:

- Information from the firm to or within the firm’s network or to service providers, and (Ref: Para. A113)

- Externally when required by law, regulation or professional standards. (Ref: Para. A114–A115)

Monitoring & Remediation

- Provides the firm with information about the design and operation of the SQM; and

- Addresses the remediation of deficiencies on a timely basis.

Requirements of the ISQM 1 Standard (and Proposed SQMS 1)

Establish a monitoring and remediation process to: (Ref: Para. A138)

- Provide relevant, reliable and timely information about the system of quality management.

- Take appropriate actions to respond to identified deficiencies and remediate them on a timely basis.

- Design and perform monitoring activities to provide a basis for the identification of deficiencies.

- Include the inspection of completed engagements in its monitoring activities. (Ref: Para. A141, A151–A154)

- Assess the competency and objectivity of individuals performing monitoring. (Ref: Para. A155–A156)

- Evaluate findings to determine whether deficiencies exist. (Ref: Para. A157–A162)

- Evaluate the severity and pervasiveness of identified deficiencies. (Ref: Para. A161, A163–A164)

- Design and implement remedial actions to address identified deficiencies. (Ref: Para. A170–A172)

- Communicate on a timely basis monitoring and remediation process. (Ref: Para. A174)