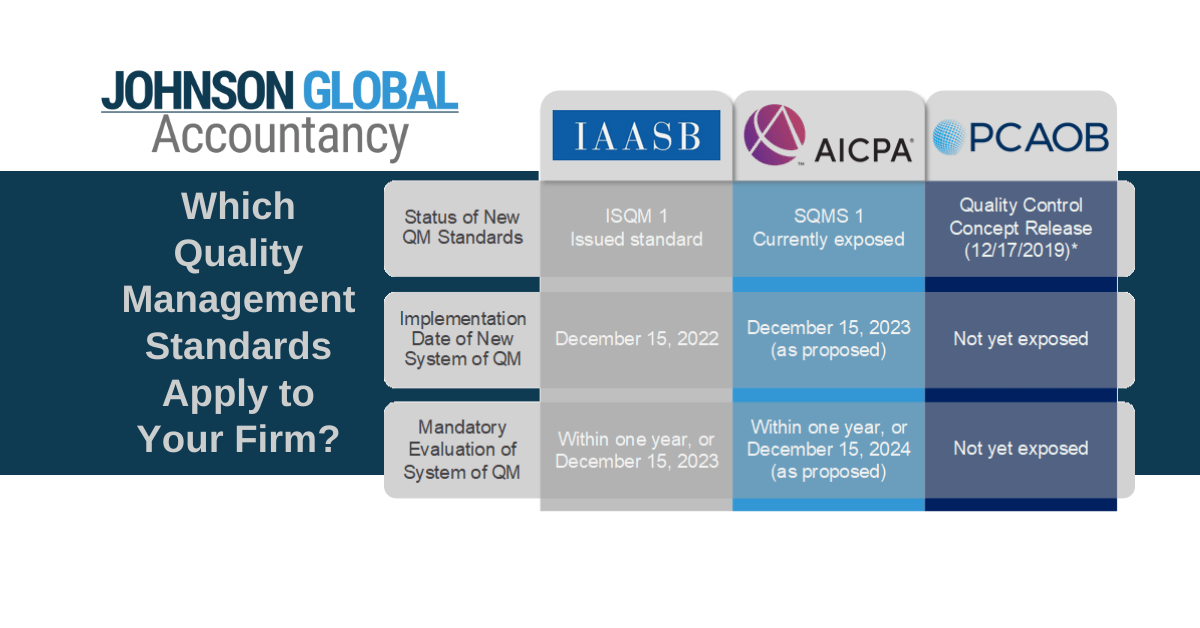

Practice Monitoring

Advisory Services for Public Company Auditors

Practice Monitoring

“Monitoring is another important element of an effective QC system. Our standards should continue to reinforce the importance of firms monitoring the quality of their overall audit practices as well as of individual audit engagements.”

- Board Member Duane DesParte

Monitoring programs are the best way for firms to ensure effective implementation of QC policies.

At Johnson Global Accountancy, we work with audit firms of all sizes - in the U.S. and abroad - to design, improve and implement monitoring programs. Through our experience in the industry, we have helped firms develop methodology for monitoring programs over all components, including complex areas related to independence, partner rotation, and internal inspections. In addition, we work with firms to design and implement the monitoring over the system of quality management to comply with new standards.

Our monitoring services include pre- and post-issuance reviews of audits for compliance over the applicable auditing and financial reporting frameworks. In this capacity, we use a risk-based and integrated approach targeting common PCAOB inspection areas and significant risks, we work with engagement teams directly to identify potential deficiencies, and advise solutions where shortfalls are identified. This proactive approach addresses issues prior to them being identified by the PCAOB or a foreign regulator during an inspection. Our expertise allows you to outsource or co-source your internal practice monitoring over all aspects of audit quality, including industry specific industries such as broker-dealer audits, and emerging industries such as cannabis and issuers involving digital assets.

What set us apart is our truly integrated approach to these services. Our Information Technology Audit Advisory Services professionals ensure ITGC’s, application controls, and firm tools and technology are considered as part of our practice monitoring services.

- DesParte, Duane M. "Improving Audit Quality through a Renewed Focus on Quality Control". PCAOB Open Board Meeting, Washington, DC, September 12, 2019.

Johnson Global Advisory

700 Flower Street #1000

Los Angeles, CA 90017

USA

+1 (702) 848-7084